- Land

- Labor

- Capital

- Two Types

- Human Capital => when people acquire skills and knowledge through experience and education

- Physical Capital => can be anything like

- Money

- Tools

- Buildings

- Equipments

- Machinery

- Entrepreneurship

_________________________________________________________________________________

Key Vocabulary

- Trade Off

- An alternative that sacrifice when we make a decision

- Scarcity reads to trade off

- Opportunity Cost

- The most desirable alternative given up as a result of a decision

- A type of trade off

- Guns or Butter

- Trade off that the government makes when choosing between wether to produce more or less military or consumer goods

- Thinking at the Margins

- Deciding wether to add or subtract one additional units of some resource

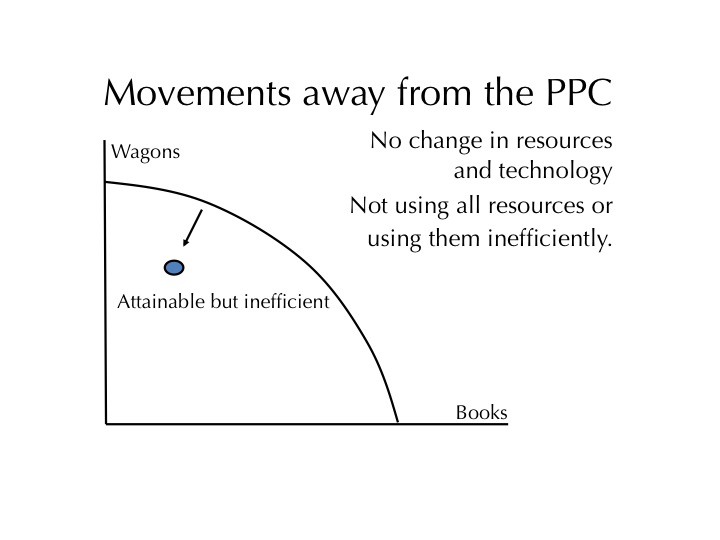

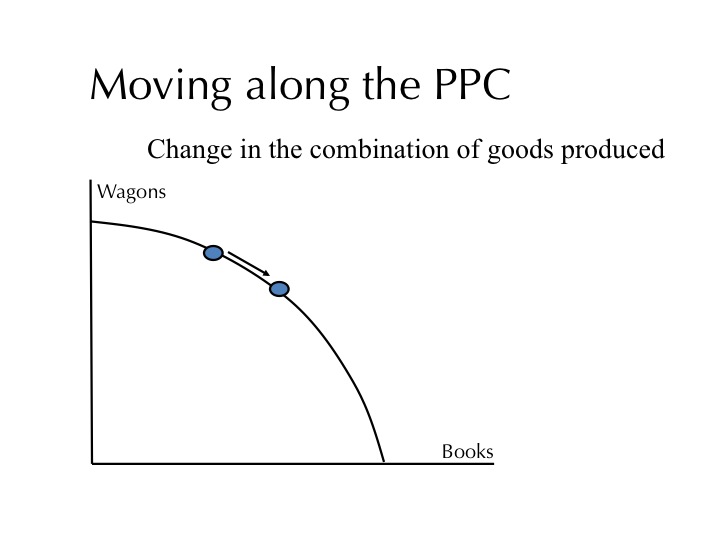

- Production Possibilities

- Graph (PPG)

- Curve (PPC)

- Frontier (PPF)

- Graphs that shows alternative ways to use an economics resources

- Efficiency

- Using resources in such a way to maximize the production of goods and services

- Increases profit

- Underutilization

- Opposite of efficiency

- Using fewer resources then an economy is capable of using

- Leads to decrease in profits

_________________________________________________________________________________

Four Key Assumptions About PPG

- Only two goods can be produced

- Full Employment of resources

- Fixed Resources

- Fixed Technology